Pension funds risk losing £200bn of returns from inflation strategies as index-linked gilts reach record high prices, PwC analysis shows

09/07/21

UK pension schemes are exposed to losses of £200bn because of their approach to securing inflation-linked returns on assets, according to PwC analysis.

Defined benefit (DB) schemes currently have £550bn tied up in gilts linked to the retail price index (RPI), making up the bulk of the whole index-linked gilt market. Most pension scheme benefits are linked to inflation to some extent, meaning there is a strong desire from pension fund trustees to cover that exposure, whether by directly investing in inflation-linked assets or other approaches. But the total UK DB pension asset base is £1,800bn, far outstripping available supply of index-linked gilts. This is leading to prices being driven up by a supply and demand imbalance.

The relentless pension scheme demand means that buying these assets now would deliver a negative real return. The same applies for any pension funds already holding index-linked gilts. Pension funds could be better off in alternative investments, which are still secure enough but deliver more value.

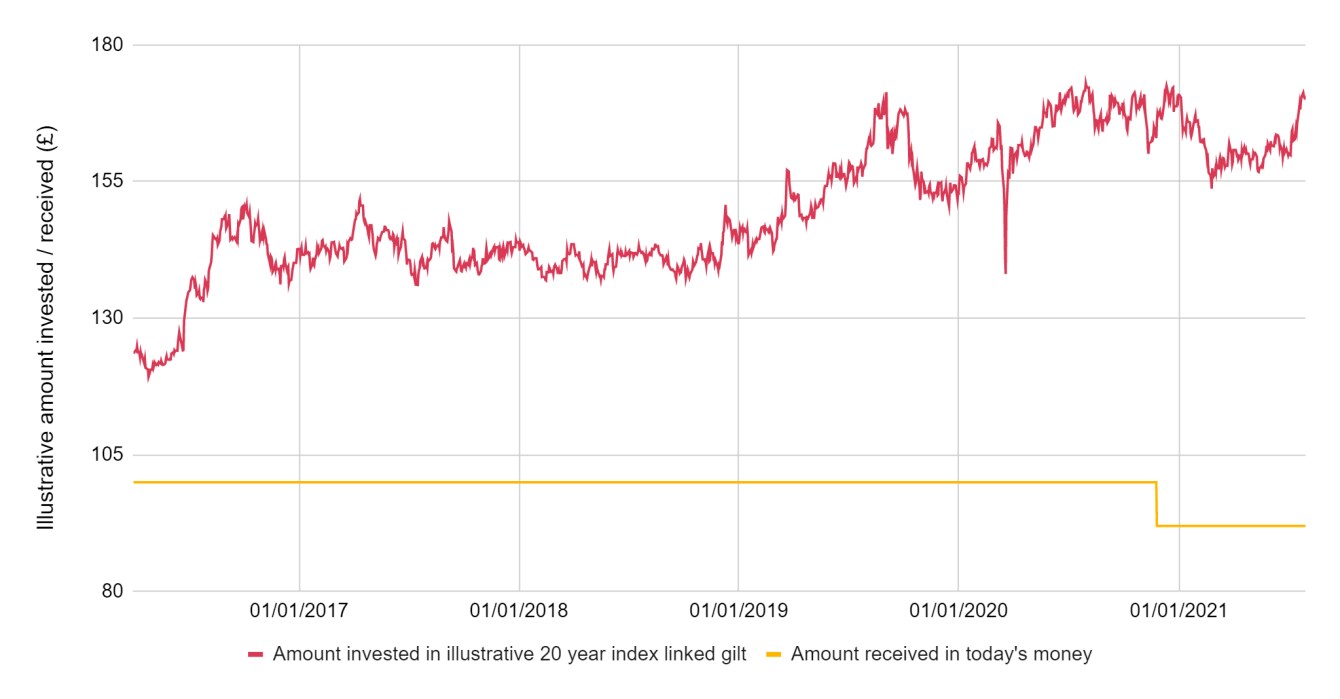

PwC analysis shows that for most of 2020, a pension scheme would have had to invest around £170 in a 20-year index-linked gilt to receive just £100 on maturity in today’s terms [see note 1 below]. This would deliver a negative real return of -2.5% per year [see note 2 below].

In November 2020, the UK Government announced that RPI would be reformed to follow the lower Consumer Prices Index (CPIH) measure from 2030. The price of index-linked gilts has not fallen to take account of reduced future maturity payments. Currently, an investor would pay £180 to receive £100 on maturity in today’s money terms. The accumulated impact of the issue across the UK DB pension universe is £200bn in lost value, according to the analysis.

Chris Venables, pensions partner at PwC, said:

“The UK Government could issue significantly more index-linked gilts to address the supply and demand imbalance, so pension schemes can achieve a reasonable level of return. Currently new issues run at only about £25bn a year. But larger new issues could exacerbate the distortions we are seeing. Investment in index-linked gilts diverts money away from other income-generating assets which can generate positive real return.

“Another option would be to make changes to pension regulations and policy to enable pension schemes to invest more freely in other income-generating assets, and not feel tied to chasing government debt. This would include ensuring the Pension Regulator’s new regime for funding pension schemes is not designed with reference to gilt yields.

“If pension schemes continue to invest in negative real-yielding assets, then either there will be insufficient funds to pay all future pensioners, or their sponsoring employers will need to pay more money to subsidise the negative real returns. This could come at a cost of more than £200bn.”

Pension fund trustees, who are responsible for their overall asset strategy, may be unaware of the value they are losing, because information they receive is not typically presented in a way which highlights it. Investment return prospects are not often shown with reference to inflation, so nothing may seem awry at first sight. However, if the returns were shown allowing for inflation, and current asset prices were shown relative to historic levels, then what is happening and what the downside risks would become more obvious.

Raj Mody, global head of pensions at PwC, said:

“It’s odd that the market has hardly reacted to the news that the RPI formula will be nearly 1% a year lower from 2030. Pension fund investors are still prepared to pay significant premiums for inflation protection via index-linked gilts, despite record price levels. As things stand, there is a downside risk to pension funding levels for schemes with strategies heavily dependent on this asset class.

“Schemes should also look again at the inflation forecasts underpinning their funding and investment targets. The market may not currently be a good predictor and this affects a whole raft of decisions for trustees and company sponsors. Of course, they have to take a holistic approach. They have to weigh up the costs and risks of protecting themselves against volatility. Plus you can’t just isolate inflation, or ESG, or any other topical issue such as the government’s recent call to action on investments. You have to develop an all-round strategy which in the end meets your outgoing pension payment commitments with a manageable level of risk.”

Additional notes:

The graph above shows the price of index-linked gilts (in red) compared to the amount the investor would receive on maturity in today’s money (in yellow), for the last five years, including the impact of the RPI/CPIH announcement. The gap shows the negative return after allowing for inflation.

The table below shows the price of index-linked gilts in column (A) vs the amount the investor would receive in real terms in column (B), and the resulting real return in column (C).

| (A) Price of 20 year index-linked Gilt (£) |

(B) Maturity amount received in real terms (£) |

(C) Investor return (after inflation) |

|

|---|---|---|---|

| 30 November 2018 (2 years before announcement) |

140 |

100 |

-1.5% pa |

30 November 2019 (1 year before announcement) |

155 |

100 |

-2.1% pa |

31 May 2020 (6 months before announcement) |

170 |

100 |

-2.5% pa |

HM Treasury announces change to RPI from 2030 (25 November 2020) |

166 |

92 |

-2.4% pa |

31 July 2021 (8 months after announcement) |

170 |

92 |

-2.5% pa |

About PwC

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 155 countries with over 284,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

© 2021 PwC. All rights reserved

Contact us