{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

Supply chain disruption is easing, but with finance still costly and difficult to secure, our analysis of 17,000 global corporations shows that working capital is still at the top of the agenda. And while large corporations are harnessing their tech-enabled management capabilities to optimise working capital, most small and mid-sized companies are still behind the curve.

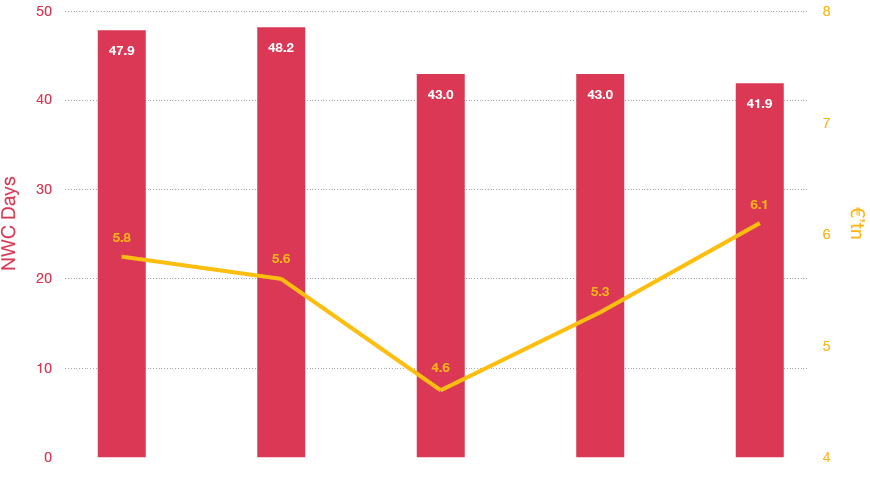

Against a backdrop of rising inflation, global revenues have continued to grow, adding to the recovery seen in 2021. Largely in line with this revenue growth, we’ve seen a continued build‑up of nominal working capital, though input costs are also increasing. Companies have managed to keep this parallel growth in their favour, resulting in a decrease of 1.1 days of cash tied up in NWC. But looking below the surface, a more mixed picture emerges.

The gradual easing in supply chain disruption has allowed companies to manage inventories more efficiently, rather than falling back on a ‘just-in-case’ stocking approach, which eases uncertainty over supplies, but uses up excessive amounts of working capital. The change of tack in inventory management is especially evident in the EU and Asia.

Explore our report

Overall working capital days, the level of net operating working capital held by businesses relative to their sales, has improved across most major economies in our study. Both DSO and DPO have fallen, with DSO dropping by 5.9%, down 3.1 days, and DPO decreasing by 6.2%, down 4.5 days. Payment terms regulation is a key driver, especially within the EU, which is limiting the ability of large buyers and sellers to dictate favourable terms with their suppliers and customers.

Explore our report

In previous years, companies tended to manage working capital by stretching supplier terms. But the latest improvements mainly stem from the asset side of working capital through better management of customer collections and closer control of inventories. Between receivables and inventories, we’ve seen an estimated €600bn reduction in nominal working capital requirements on the asset side, relative to what we would have seen on prior year trends. More than €250bn of this has come from the EU alone.

Explore our report

The improvements in NWC have been primarily driven by large companies. Both medium- and small-sized companies actually saw a deterioration in NWC days, 3.6 and 3.2 days respectively. This suggests that large companies are the primary beneficiaries of technological advances, which support a reduction in working capital. As boutique and midmarket technology players continue to gain a foothold, we expect many small and mid-sized companies to acquire the technology they need.

Explore our report

Although the improved efficiency of Working Capital Management (WCM) is encouraging, the challenge of attracting and retaining enough staff to run key working capital processes continues. Automation and digitisation can cover a lot of the work and free up precious time. But technology isn’t a silver bullet. With so much choice, selecting the right tools and defining a solid business case can be challenging. In turn, implementation impacts on a wide range of stakeholders, underlining the importance of organisation-wide understanding, buy-in and change management.

Explore our reportPwC’s operational and specialist Working Capital team supports company management to realise cash improvements at pace, improve operational processes, deploy supporting technology, and drive organisational transformation.

Partner, Working Capital Management & Value Creation, PwC United Kingdom

Tel: +44 (0)7725 633420

Partner, Working Capital Management and Execution Managed Services, PwC United Kingdom

Tel: +44 (0)7717 782240