Summary

The financial technology (FinTech) sector continues to evolve. After several years of excitement about the sector’s potential to change the face of financial services, some of that change is starting to become real, with leading FinTechs commercialising their services at pace, both independently and in collaboration with incumbents.

Inevitably, early expectations have had to be shifted. Where FinTech companies were once seen as a threat to the incumbents, promising disruption in an industry suffering from a loss of customer trust, the emphasis has shifted to collaboration. FinTech now also has a lens on technologies that address operational challenges as well as customer expectations.

Advances in areas such as artificial intelligence, big data and blockchain offer huge opportunities in this context. These areas are opening up new avenues of growth and delivering greater operational efficiency and productivity, while all the time focusing on specific customer pain points.

From our position at the heart of the FinTech ecosystem, Startupbootcamp and PwC enjoys a unique view of emerging trends in this sector. Based on the qualitative intelligence and experience gleaned from this work over the past 12 months, as well as quantitative insight from the programmes’ application data and UK funding data, this report aims to provide key insights into the evolution of the FinTech sector.

Steve Davies, PwC and Francisco Lorca, Startupbootcamp FinTech London discuss a year in FinTech.

Key findings

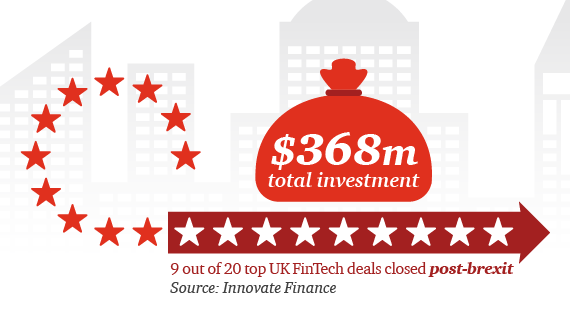

Despite Brexit, the UK should remain a global FinTech leader.

Economic and political uncertainty poses a threat, but the European FinTech sector is in a healthy position, led by the UK. Regulators across Europe are following the UK’s example as they seek to foster an agile environment conducive to innovation; the UK, meanwhile, has built FinTech bridges with a growing number of international markets and continues to attract investors from territories such as Canada and Japan. Also despite many blaming the large drop in investment in the UK on the Brexit referendum, nine of the top 20 UK FinTech deals closed posed Brexit, with the total investment for this period tallying $368m.

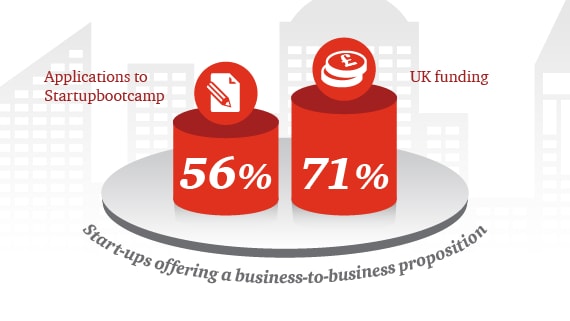

More start-ups want to work with existing financial services businesses. Growing understanding of each other’s cultures and working practices has seen FinTech companies and incumbents work together much more frequently. Start-ups offering a business-to-business proposition accounted for 56% of applications to Startupbootcamp last year and for 71% of UK funding; their focus is very often on improving incumbent’s internal operating processes.

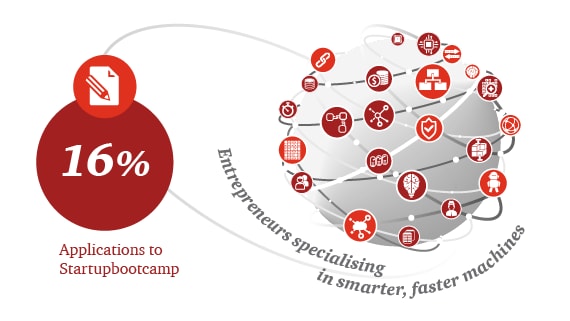

The most successful artificial intelligence and machine learning advances put the customer at the centre. FinTech companies pioneering these technologies have moved towards a design-led approach. The increasing volume of open source material available to start-ups has enabled them to focus on technological advances from the perspective of specific customer problems.

Serving the unserved has become a key priority for start-ups globally. FinTech companies are aware and concerned about the unfairness and opportunities that arise from a huge number of people that are not served by the financial service sector. More than one in 10 applications to Startupbootcamp FinTech 2016 (12%) came from start-ups aiming to tackle issues of financial inclusion and wellbeing. Traditionally a focus in developing countries, UK and European FinTech companies are increasingly engaged with these issues too.

Great change has taken place in the collaboration between start-ups and incumbents, but these are only the first steps as more work to be done. Much progress has been made as FinTech companies and incumbents have got to know each other better, but the search for the perfect collaboration model continues. Up till now most projects end on proof-of-concept or pilot studies. The next phase of growth is to turn more of these into real business. Too many corporates are struggling to measure success in FinTech.

More start-ups want to work with existing financial services businesses. Growing understanding of each other’s cultures and working practices has seen FinTech companies and incumbents work together much more frequently. Start-ups offering a business-to-business proposition accounted for 56% of applications to Startupbootcamp last year and for 71% of UK funding; their focus is very often on improving incumbent’s internal operating processes.

The most successful artificial intelligence and machine learning advances put the customer at the centre. FinTech companies pioneering these technologies have moved towards a design-led approach. The increasing volume of open source material available to start-ups has enabled them to focus on technological advances from the perspective of specific customer problems.

Serving the unserved has become a key priority for start-ups globally. FinTech companies are aware and concerned about the unfairness and opportunities that arise from a huge number of people that are not served by the financial service sector. More than one in 10 applications to Startupbootcamp FinTech 2016 (12%) came from start-ups aiming to tackle issues of financial inclusion and wellbeing. Traditionally a focus in developing countries, UK and European FinTech companies are increasingly engaged with these issues too.

Great change has taken place in the collaboration between start-ups and incumbents, but these are only the first steps as more work to be done. Much progress has been made as FinTech companies and incumbents have got to know each other better, but the search for the perfect collaboration model continues. Up till now most projects end on proof-of-concept or pilot studies. The next phase of growth is to turn more of these into real business. Too many corporates are struggling to measure success in FinTech.

More start-ups want to work with existing financial services businesses. Growing understanding of each other’s cultures and working practices has seen FinTech companies and incumbents work together much more frequently. Start-ups offering a business-to-business proposition accounted for 56% of applications to Startupbootcamp last year and for 71% of UK funding; their focus is very often on improving incumbent’s internal operating processes.

The most successful artificial intelligence and machine learning advances put the customer at the centre. FinTech companies pioneering these technologies have moved towards a design-led approach. The increasing volume of open source material available to start-ups has enabled them to focus on technological advances from the perspective of specific customer problems.

Serving the unserved has become a key priority for start-ups globally. FinTech companies are aware and concerned about the unfairness and opportunities that arise from a huge number of people that are not served by the financial service sector. More than one in 10 applications to Startupbootcamp FinTech 2016 (12%) came from start-ups aiming to tackle issues of financial inclusion and wellbeing. Traditionally a focus in developing countries, UK and European FinTech companies are increasingly engaged with these issues too.

Great change has taken place in the collaboration between start-ups and incumbents, but these are only the first steps as more work to be done. Much progress has been made as FinTech companies and incumbents have got to know each other better, but the search for the perfect collaboration model continues. Up till now most projects end on proof-of-concept or pilot studies. The next phase of growth is to turn more of these into real business. Too many corporates are struggling to measure success in FinTech.

More start-ups want to work with existing financial services businesses.

Growing understanding of each other’s cultures and working practices has seen FinTech companies and incumbents work together much more frequently. Start-ups offering a business-to-business proposition accounted for 56% of applications to Startupbootcamp last year and for 71% of UK funding; their focus is very often on improving incumbent’s internal operating processes. The emergence of enabling businesses reflects increasing recognition of the potential for FinTech start-ups technologies and solutions to confront some of the most pressing challenges facing incumbent financial services providers – including their high cost-to-income ratios, which have plagued many large banks for some years now.

The most successful artificial intelligence and machine learning advances put the customer at the centre.

FinTech companies pioneering these technologies have moved towards a design-led approach. The increasing volume of open source material available to start-ups has enabled them to focus on technological advances from the perspective of specific customer problems. The percentage of applications to Startupbootcamp from entrepreneurs in the Smarter, faster machines category was 16% in 2016, as the approach of design thinking evolves. We found that our applications in this area mainly focussed on artificial intelligence (AI) and machine learning. This year FinTech companies in this space are identifying customer problems to be solved and then considering how technology might help. This is exciting: technology should enable organisations to create value, for both customers and themselves, and the greater the focus on where that value is required, the greater the chances of success.

Serving the unserved has become a key priority for start-ups globally.

FinTech companies are aware and concerned about the unfairness and opportunities that arise from a huge number of people that are not served by the financial services sector. More than one in 10 applications to Startupbootcamp FinTech 2016 (12%) came from start-ups aiming to tackle issues of financial inclusion and wellbeing. In the past, we have seen the majority of these companies coming from developing regions trying to solve the issue of financial inclusion. This has not changed with one fifth of these companies coming from the African region (mainly solving issues around payments and money transfers). However, we have also seen strong growth in this area from within the UK and Europe (63% of all the financial inclusion and wellbeing applicants), mainly focussing on financial wellness. This showcases that this is an issue that is growing across the world.

Great change has taken place in the collaboration between start-ups and incumbents, but these are only the first steps as more work to be done.

Much progress has been made as FinTech companies and incumbents have got to know each other better, but the search for the perfect collaboration model continues. Until now most projects end on proof-of-concept or pilot studies. The next phase of growth is to turn more of these into real business. Too many corporates are struggling to measure success in FinTech. Where progress needs to be made with incumbent firms is the need to have business led R&D with a focus on implementation. Nevertheless, the direction of travel is to be welcomed and should accelerate.

Related content

Contact us