Pillar 2: A pathway forward

April 2022

Overwhelmed! That might just sum up how most were feeling when reading through the OECD Pillar 2 model rules. A new set of rules, running parallel to existing domestic accounting and tax reporting obligations, is expected to apply from 2023 with many jurisdictions also considering implementing Domestic Minimum Tax (QDMT) regimes and introduced at different times across the world.

While many organisations within the scope of the Pillar 2 rules may not have any top-up tax to pay, the rules nonetheless usher in a new frontier of tax reporting and compliance - and the process, data and technology challenges that go with it.

So you’ve read the model rules, you’ve looked at your global footprint and identified the risk areas, perhaps even been surprised by some of the countries with exposure to top-up tax. You realise the start date in the UK could be for accounting periods ending after April 2023 and think, where to from here?

Some questions to consider as you’ve evaluated the impact of the model rules:

- Have you undertaken any modelling (high level or detailed) around the impact of Pillar 2 on your business?

- Do your finance systems have the data required to complete the GloBE calculation and how easy will it be to change this?

- Is the tax reporting process (and the technology that drives it) fit for purpose going forward?

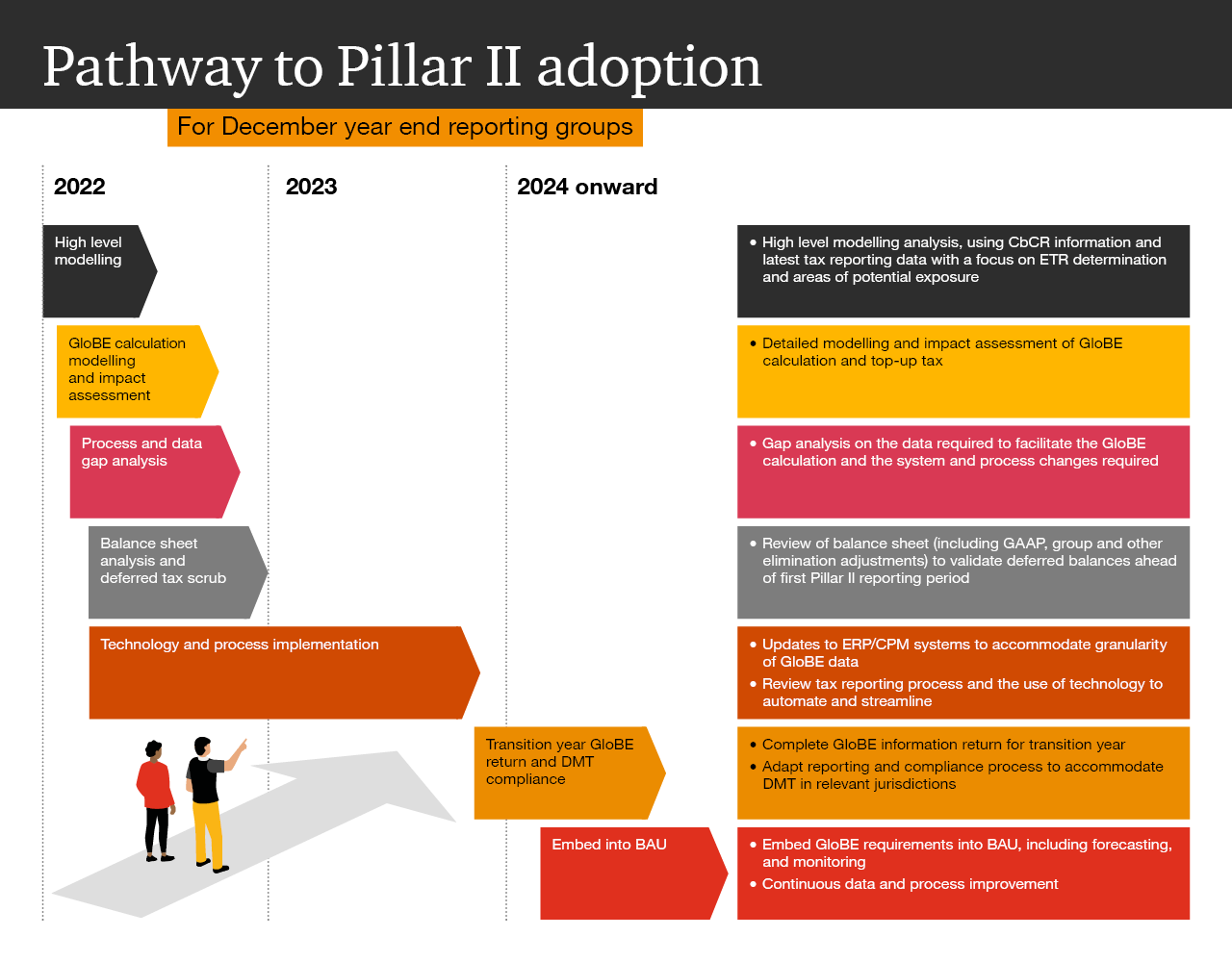

The roadmap under Pillar 2

It’s important for each group to map out their route to the end state of Pillar 2 reporting and compliance and break the seemingly impossible into smaller, bite-sized phases. We’ve plotted these phases on a roadmap as an illustrative example below:

- High level modelling

- GloBE calculation modelling & impact assessment

- Process & data gap analysis

- Balance sheet analysis & deferred tax

- Technology & process implementation

- Transition year GloBE return & DMT compliance

- Embed into Business as Usual

High level modelling

Leveraging the latest CbCR or summarised tax provision data, groups are able to ascertain a very quick snapshot of the jurisdictions at risk from a minimal time investment.

GloBE calculation modelling & impact assessment

Completing the GloBE calculation in detail will shine a light on areas of risk, both from a potential top-up tax and data and process perspective and our experience thus far has shown the results are often not intuitive. The nature of the adjustments required for the GloBE calculation are different to what is required for tax accounting, and some of the data may not be easily available or split out by entity or jurisdiction. For example, we expect the traditional use of a handful of elimination or group adjustment ‘entities’ to capture top-sides within the group accounts to diminish, with the need to identify and possibly eliminate intra territory consolidation adjustments as part of the GloBE calculation. Our Market Tax Analyser (MARTA) tool can give you a sense of the potential top up tax liabilities that may be due.

Your impact assessment should also look to identify areas where there may be technical uncertainty on the application of the rules to your fact pattern and to determine how those need to be addressed.

Process & data gap analysis

Understand the data you need and compare that with the data available today - the analysis of those missing pieces will be crucial to drive changes in the technology and processes across finance and tax. It’s important to remember that any DMT regime may be calculated on a basis more closely to GloBE principles rather than statutory or local tax requirements. This means that local processes will need to adapt significantly in order to comply. Where change is needed, the gap analysis should be the critical component of the tax function’s business case for investment.

Balance sheet analysis & deferred tax

Closing balances this year will be the opening balances for the first year of Pillar II, so the correctness and accuracy of deferred tax positions is critical due to the requirement to recast these at the 15% rate. Undertaking a detailed review before Pillar II comes into effect could save on large prior year adjustments or unnecessary top-up tax in the future.

Technology & process implementation

Update source EWP systems where necessary to address data gaps. Can changes be made to collect the data points you need as finance data is entered rather than having to to back end rework? Pillar 2 reporting is a top-down approach requiring bottom-up data, so implementing the appropriate tax reporting technology, augmented with additional modelling solutions if required, will yield benefit across the end-to-end tax reporting lifecycle and ease some of the burden of Pillar 2 compliance.

Transition year GloBE return & DMT compliance

On top of the GloBE return (and any other DMT returns required), undertaking forecasting at relevant intervals will mean fewer surprises by the end of the year and allow the business to more accurately report or disclose any top-up tax implications. Any new process has teething issues, so the process should ideally not be designed around a single, annual process conducted at a time when any errors will need to be corrected by prior year adjustments. Disclosure and filing of the relevant returns must be in line with the relevant schemas.

Embed into Business as Usual

There will be learnings over the first couple of years of Pillar II and continuous improvement on data, process and technology is essential in achieving an efficient reporting and compliance cycle. Synergies will be found across tax provisioning, forecasting, GloBE and DMT regimes (especially as more jurisdictions introduce these) through the use of technology for greater automation and transparency.

As overwhelming as Pillar II appears, its adoption can be managed effectively with planning and a roadmap for what your organisation needs to do to be ready. Meeting these requirements is going to be a combination of modelling, reporting and compliance - exploring how these interact in conjunction with, rather than separate from, the existing process, data and technology will provide the strategic framework for what will eventually become just another obligation of the tax function.

Contact us

Follow us