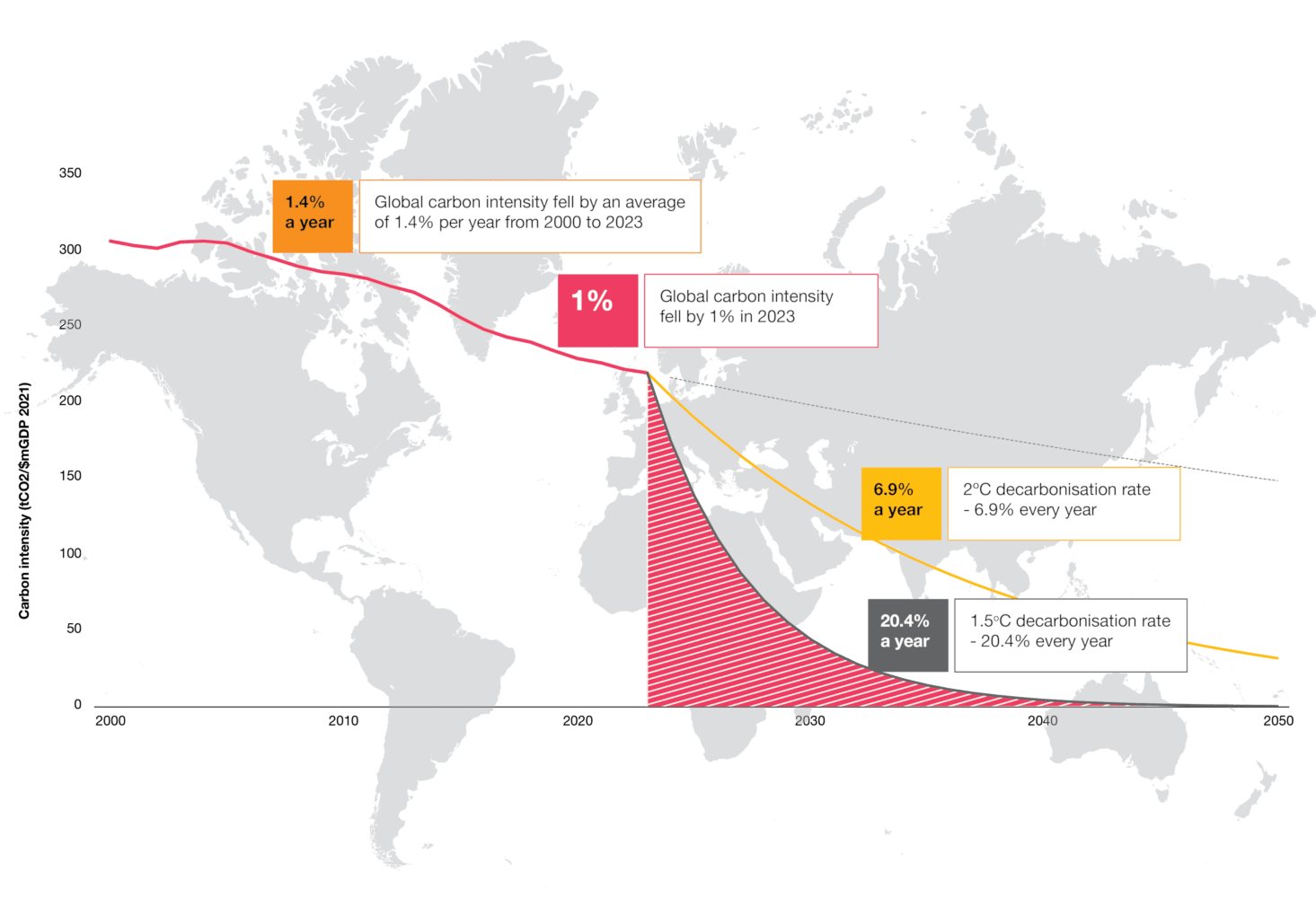

This year's analysis shows the reduction in carbon intensity has stalled to its lowest level in over a decade, at just 1.02%.

This reflects a troubling stall in the progress we have made in decoupling economic growth from emissions.

The Net Zero Economy Index is our annual indicator of the progress made in reducing energy-related CO2 emissions and decarbonising economies. With a global decarbonisation rate of only 1.02% in 2023, the world must now decarbonise twenty times faster to limit warming to 1.5°C above pre-industrial levels.

The likelihood of overshooting this threshold is fast becoming reality. Even limiting warming to 2°C – the lowest end of the Paris Agreement’s ambition – requires a step change in progress with an annual decarbonisation rate of 6.9%.

Incremental progress is being made. There’s been strong growth in renewable energy capacity. However, with energy demand growing, our reliance on fossil fuels continues to rise and fossil fuels still dominate the energy mix.

Reducing energy intensity and more effectively managing demand offers an opportunity for business and government to accelerate action. The private sector can lead in deploying energy efficiency technologies, adopting circular business models and implementing advanced manufacturing processes. Governments can enhance this effort by aligning public policy with private innovation, an important step towards a secure and sustainable energy future.

Current trends suggest an ever-widening gap between ambition and action. The window for action is closing. Immediate and sustained efforts are crucial to turn the incremental progress made into exponential change and ensure a sustainable and resilient future for all. It’s time to act.

global decarbonisation rate, the lowest in over a decade

“If we don't take bold action, we risk exceeding 1.5°C of warming and the greater the overshoot, the more severe the impact. Despite these warnings, the gap between goals and actions is growing. Without global cooperation, the possibility of keeping warming within safe limits will disappear. To achieve the necessary changes, we must expand the use of renewable energy, manage energy demand better, and increase financial and technical support for a fair transition.”

Emma Cox, Global Climate Leader, PwC UK

Smallest decrease in carbon intensity since 2011.

The greater the overshoot, the more severe the impact.

Growth in renewables not keeping pace with energy demand.

Financial and technological support is needed for a just transition.

Urgent action needed on energy efficiency and demand management

Policy needs to promote innovation and agility to manage energy demand

For details on our methodology and key metrics - including fuel factor and energy intensity - find out more in the methodology and metrics section below.

The Net Zero Economy Index tracks the decarbonisation of energy-related CO2 emissions worldwide.

The analysis is underpinned by The Energy Institute’s Statistical Review of World Energy, which reflects energy consumption per fuel type per country and CO2 emissions from energy, process emissions, methane and flaring.

Our data sources include: The Energy Institute, IEA, World Bank, OECD, PwC

AFOLU (Agriculture, Forestry and Other Land Use) emissions are excluded from this analysis. No carbon sequestration is accounted for in the Net Zero Economy Index analysis. As a result, this data cannot be compared directly with national emissions inventories.

G7 comprises: Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States

E7 comprises: Brazil, China, India, Indonesia, Mexico, Russia, and Turkey

G20 comprises: G7 countries, E7 countries, Argentina, Australia, Korea, Saudi Arabia, South Africa, and the EU

More detail on methodology can be found in the downloadable pdf.

The primary purpose of the Net Zero Economy Index is to calculate national and global carbon intensity (CO2e / GDP), and track the rate of change needed by 2050 to limit warming to 1.5°C.

To do this, we use the IPCC carbon budget to calculate how much emissions need to be reduced in the future, and divide this by the projected increase in GDP.

This allows us to see the amount emissions must reduce to maintain projected GDP growth, providing insight to the scale of efforts required to decouple emissions from economic growth.

The fuel factor (CO2e / energy) measures how much CO2e is emitted per unit of energy consumed. Put simply, how green the energy consumption is.

It indicates a country’s shift in energy mix towards renewable energy sources, and can reflect movements away from the most highly emitting fossil fuels (such as coal).

For each unit of energy consumed, different fossil fuels will release differing amounts of CO2e emissions. For each unit of energy consumed from a renewable source, emissions will be reduced to negligible, or zero, therefore reducing the fuel factor toward zero.

Energy intensity (energy / GDP) measures the amount of energy consumed per unit of GDP generated.

It shows us how much energy is needed to generate a given amount of GDP.

Energy intensity is impacted by factors including: energy efficiency, in the form of energy efficiency policies or technological advances enabling efficiency; energy pricing mechanisms; shifts in regional population and demographics; changes in the composition of an economic sector’s output; maximising economic output per unit spend on energy usage; investment in new, more efficient technology and infrastructure; and climatic influences on energy usage.