Milton Keynes is UK’s fifth top-performing city

- Milton Keynes remains in UK’s top-performing cities for the fourth year in a row

- Milton Keynes is one of 11 cities to see a decline in scores driven by top performing cities’ improvement hitting a relative ceiling, falling one place in the national rankings to fifth

- Milton Keynes joins neighbouring cities Oxford and Cambridge in top performing cities again - building the case for investment in Oxford-Milton Keynes-Cambridge Arc

- Skills amongst the working-age population and new business formation have driven the largest improvements in average scores.

Milton Keynes has maintained its position as a top-performing UK city, on PwC’s Good Growth for Cities 2019 index. However it has seen a decline in its overall index score, slipping from fourth highest performing and fastest improving in last year’s index, to fifth highest performing this year. It was one of 11 cities to see a decline in their overall scores relative to the previous index, driven partially by the improvement, especially for top performers like Milton Keynes, hitting a relative ceiling.

Published today (12 November 2019), the annual Good Growth for Cities 2019 sets out to show there’s more to economic well-being than just measuring GDP. The index measures the performance of 42 of the UK’s largest cities, England’s Local Enterprise Partnerships (LEPs) and ten Combined Authorities, against a basket of 10 factors which the public think are most important when it comes to economic well being. These include jobs, health, income and skills, as well as work-life balance, house-affordability, travel-to-work times, income equality, environment and business start-ups.

Milton Keynes scores particularly highly in jobs and income distribution, but below average on variables such as work-life balance, house price to earnings, and transport. Milton Keynes saw the biggest increase in score since 2015-17 in the work-life balance measure, and the largest decrease in score over the same period was in health.

The price of success for Milton Keynes is housing affordability, as it is ranked in the index as the seventh city for highest house prices to earnings ratio - behind London, Cambridge and Bristol.

This year’s index sees nine in ten cities in 2016- 2018 having scores higher than the average for all cities in our base year of 2011-2013, highlighting the rate of recovery since the financial crisis. There is strong employment growth, which reflects the continued decline in unemployment, as well as improvements in work-life balance, perhaps as a result of more flexible working patterns becoming more acceptable.

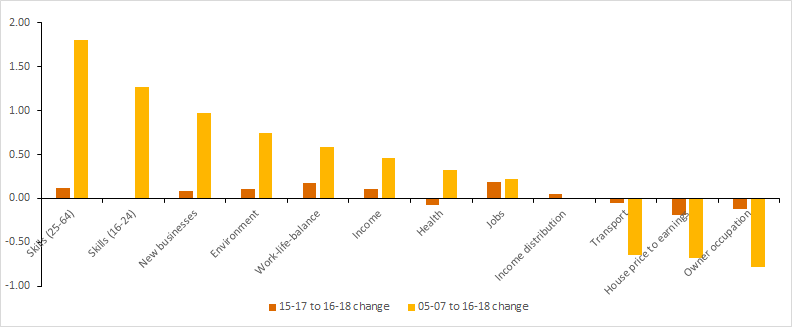

The long term data suggests that performance over time on the index is not driven by a city’s starting position, but rather by a combination of local and national improvements in the economy. The figure below shows the change in average good growth index scores by variable across all cities since 2005-07 and 2016 - 18. Skills amongst the population of 16-64 year olds, alongside the number of new businesses created have seen the largest improvements in average scores over the period, however housing affordability and owner occupation have deteriorated over the period, alongside rising average commuting times.

Average change in good-growth scores between 2005-07 and 2016-18.

The short term data tells a different story, as 11 cities in the index have witnessed a decline in their score relative to the previous index – this is partly driven by the fact that improvement (especially for top performers) has hit a relative ceiling. However, the price of success has become increasingly evident, with declines in transport and housing highlighting the ongoing infrastructure challenges faced by UK cities. There has also been a decline in skills among young people (16-24) and a decline in overall health.

Office senior partner for PwC in Milton Keynes, Sam Taylor, commented:

“Despite a backdrop of uncertainty local leaders have had significant success in delivering good growth in Milton Keynes and the wider region. Our research shows the need to take a comprehensive approach to growth, focusing on improving productivity to compete on a global stage, but also on ensuring fairness and inclusive growth so that people and places don’t feel left behind.

“It is testament to the collaboration and entrepreneurial spirit across public and private partnerships in the region, that Oxford, Cambridge and Milton Keynes are all in the top 10 performing cities. This demonstrates we have three fantastic pillars to continue to build our Arc vision on by continuing to attract investment in business, infrastructure, research & development and education. Our shared aspirational vision for the Arc will see a stream of businesses and infrastructure connecting these top performing cities. However, as is seen in many cities’ performance this year, maintaining the momentum of growth is dependant on continued investment in infrastructure through key projects, such as the bid for Milton Keynes University, and road and rail infrastructure across the Arc.”

All Local Enterprise Partnerships (LEPs) have seen absolute increases in environment scores but absolute decreases in owner occupation scores since 2015-17. Skills amongst people aged 25+ was the variable that saw the largest improvement compared to the 2015-17 index, whilst house price to earnings measure saw the largest decline. The South East Midlands LEP (SEMLEP) area, which Milton Keynes sits in, was ranked 18th out of 37 LEP areas, and saw the biggest increase in its work-life balance score, and the largest decrease in house price to earnings.

PwC partner and local government leader Jonathan House, commented:

“In an era of political, technological and environmental disruption, cities and regions that want to get ahead, need to do things differently. Even with the uncertainty of Brexit, over the last year, local leaders have had significant success in delivering good growth in their cities and regions.

“Local leaders need to take a broad view on what economic success means, focusing on the outcomes they want to achieve in terms of inclusive growth, community resilience and improved experience, and crucially, having a plan to translate those ambitions into reality.

“Skills amongst the working age population, alongside the number of new businesses created, have seen the largest improvements; this is a result of leaders focusing on building new opportunities and investing in the talent of their city and region.

“The UK’s cities are known globally for their skills, innovation and entrepreneurial spirit. Our most successful cities don’t compete against other UK cities, they compete against cities across Europe, the Middle East and the US. As the UK’s position on the world stage shifts, cities and regions will need to reposition themselves too, and consider how they can stand out and compete globally, improve productivity and support innovation, while also creating places that are fair and inclusive. ”

National performance

Oxford and Reading remain the top-performing UK cities, followed by Southampton in third place.

Bradford emerged as this year’s top improver, driven by jobs, work-life balance and skills amongst its 25+ year olds. Bradford has experienced a large reduction in its unemployment rate, measured at 4.1% in 2018 compared to 10% in 2015. The city also demonstrated moderate improvements in work-life balance, health, environment and skills amongst the adult population.

This year’s index has seen continued improvements in index scores across the UK, driven in particular by falling unemployment rates and increases in new business per head. Whilst there have been strong job improvements, these have reflected a continued decline in house price to earnings ratio. More affluent cities typically have higher overall scores than their less affluent peers, however this also means they typically have lower scores in the areas of housing affordability and ownership, particularly in the case of London.

Previous PwC research found that for those who can afford to buy a house in England, it will cost, on average, around £25,000 to live near the best performing state schools. In addition, PwC’s July edition of the UK Economic Outlook also found that rental affordability ratios in the UK have deteriorated, with some key workers now priced out of the rental market in London and the South East.

PwC chief economist John Hawksworth, said:

“Our long term analysis shows that good growth improvements across the UK since 2005 have been largely driven by skills and new business creation. As the economy and world of work transforms, ensuring people are equipped with the digital and other skills they need for future jobs will remain critical to sustaining these improvements.

“But there are also less positive long term trends, particularly relating to deteriorating housing affordability and ever longer commuting times. These issues will require sustained investments in affordable housing supply and transport infrastructure to address.

“This year’s index results has shown continued broad-based improvements across most UK cities, but there are also signs that progress has plateaued, particularly among top performing cities in the index where unemployment rates were already very low. Increased investment in health, education and skills will be important to drive further improvements in the index now that the post-crisis task of reducing unemployment rates has been met in most parts of the country. ”

The top-10 highest ranked cities in our latest index, which relates to the period 2016-2018, and the most improved since last year’s index were:

Highest ranking cities |

Top 10 improvers |

Oxford |

Bradford |

Reading |

Liverpool |

Southampton |

Norwich |

Bristol |

Newcastle |

Milton Keynes |

Cardiff |

Aberdeen |

Swansea |

Edinburgh |

Wolverhampton |

Swindon |

Brighton |

Cambridge |

Hull |

Leicester |

Manchester |

2019 full list of index ranking

Find out more and access the full report at www.pwc.co.uk/goodgrowth